Going solar is one of the smartest financial moves a Florida homeowner can make, but the upfront cost stops a lot of people before they even get a quote. That’s where searching for solar financing near me becomes the logical next step. The good news? You have more options than you probably realize, from solar-specific loans and leases to government-backed programs designed to make clean energy accessible without draining your savings account.

The challenge is sorting through those options. Not all solar loans are created equal, and the difference between a great financing deal and a mediocre one can mean thousands of dollars over the life of your system. Interest rates, loan terms, dealer fees, and eligibility requirements vary widely depending on the lender, and some offers that look attractive upfront carry hidden costs that eat into your savings.

At Advance Solar & Spa, we’ve helped Florida homeowners and businesses navigate solar financing for over 40 years and across more than 50,000 installations. Our certified solar consultants work with you to understand not just which system fits your roof, but which financing structure actually makes sense for your budget and goals. We’ve seen every type of loan, lease, and incentive program out there, and we know what works.

This guide breaks down exactly how to find the best solar financing options available to you, what to watch out for, and how to compare lenders so you can go solar with confidence and keep more money in your pocket from day one.

What solar financing means in 2026

Solar financing in 2026 looks meaningfully different from what it did even three years ago. Interest rates have shifted, more lenders now offer solar-specific loan products, and the range of structures runs from simple personal loans to manufacturer-backed programs with deferred payment windows. Understanding the full landscape before you start comparing offers gives you a real advantage when deciding what actually qualifies as a good deal for your situation.

The main financing types available today

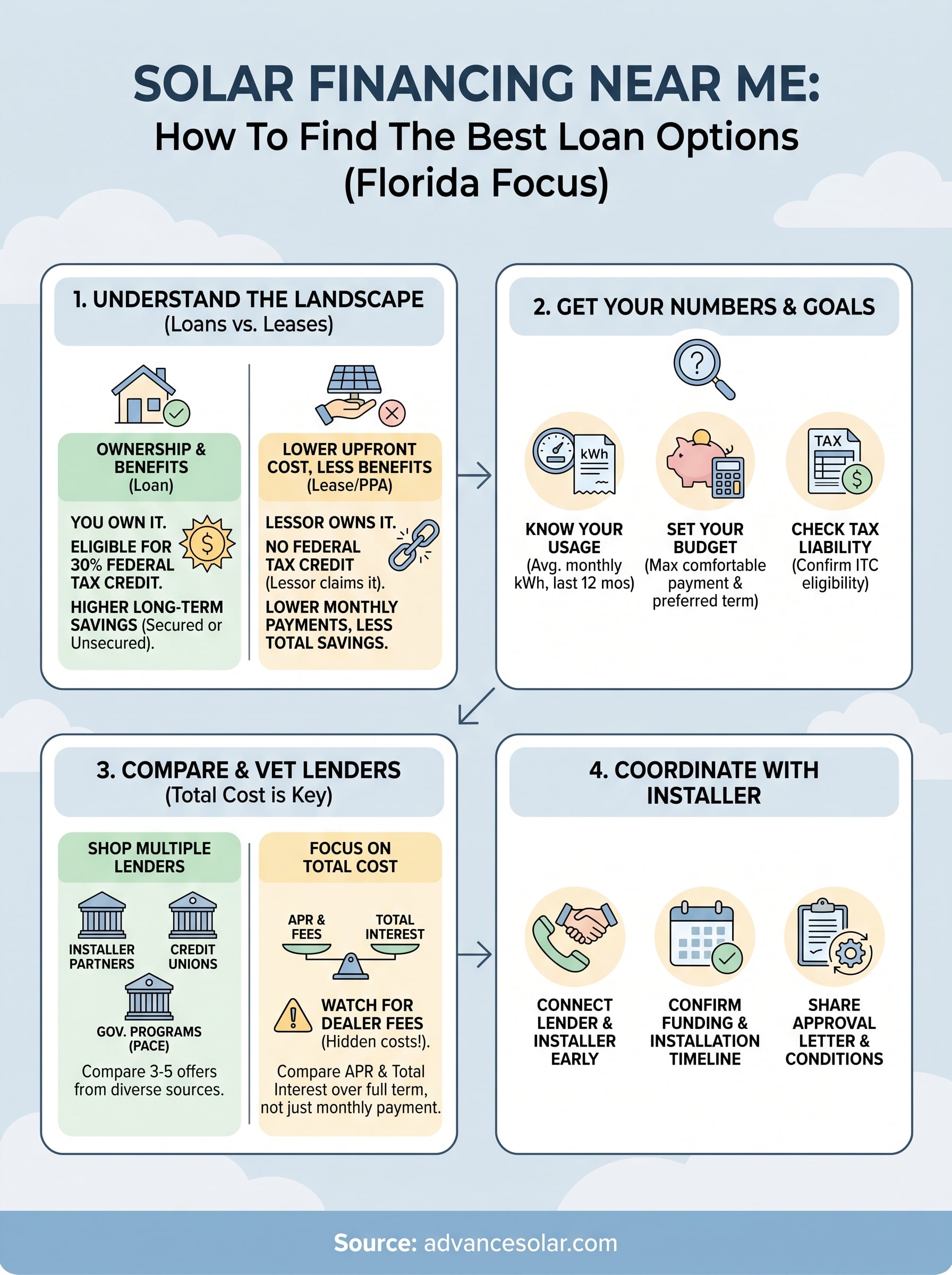

Most homeowners researching solar financing near me will encounter four core product types. Each works differently and carries its own trade-offs around ownership, tax credit eligibility, and total long-term cost.

| Financing Type | You Own the System | Eligible for Federal Tax Credit | Typical Term |

|---|---|---|---|

| Solar loan (secured) | Yes | Yes | 10-25 years |

| Solar loan (unsecured) | Yes | Yes | 5-12 years |

| Solar lease | No | No (lessor claims it) | 20-25 years |

| Power purchase agreement (PPA) | No | No (lessor claims it) | 20-25 years |

Secured solar loans use your home equity as collateral and typically carry lower interest rates. Unsecured loans require no collateral but come with higher rates and shorter terms. Leases and PPAs eliminate upfront costs entirely, but you give up ownership, which means the installer or leasing company claims the federal tax credit instead of you.

How federal and state incentives change the math

The federal Investment Tax Credit (ITC) currently lets you deduct 30% of your total system cost from your federal tax liability. That includes equipment, installation labor, and battery storage when charged by solar. On a $30,000 system, that is a $9,000 reduction in what you owe the IRS, which compresses your break-even timeline considerably.

The 30% federal tax credit only applies to you if you own the system through a cash purchase or a solar loan. Leases and PPAs disqualify you from claiming it entirely.

Florida adds two more layers on top of the federal incentive. Solar equipment is exempt from state sales tax, and the added home value from a solar installation is exempt from property tax reassessment. Together, these state-level benefits make financing a system in Florida more financially compelling than in most other states.

Why the lender you choose matters as much as the loan

Not every lender operates transparently, and the difference between them shows up in the details most people overlook. Dealer fees, sometimes called origination fees or finance charges that the lender bills to the installer, often get rolled into your total system cost without being clearly disclosed. Some installers pass that fee straight to you, inflating your price by 15-30% above what you would pay in cash.

Your goal is to understand the all-in cost of the loan, including principal, total interest over the full term, and any fees embedded in the financing structure. A loan advertised at 2.99% APR paired with a heavy dealer fee can easily cost more than a straightforward loan at 6.99% APR with no added fees. Comparing offers based on total cost rather than monthly payment is the only way to identify a genuinely competitive deal.

Step 1. Get your solar numbers and goals

Before you start comparing any lenders or searching for solar financing near me, you need a clear picture of two things: what size system you actually need and what you can realistically afford each month. Skipping this step leads most homeowners to either overborrow for a system larger than they need or underborrow and end up with a system that barely moves the needle on their utility bill.

Know your current electricity usage

Your electricity bills hold the data that drives every solar calculation. Pull your last 12 months of utility statements and find your average monthly kilowatt-hour (kWh) usage. Most Florida utility providers list this directly on the bill or in your online account dashboard. Your annual kWh total tells a solar installer how large a system you need to offset your consumption meaningfully.

Use this simple template to organize what you need before any installer conversation:

| Data Point | Where to Find It | Your Number |

|---|---|---|

| Average monthly kWh usage | Utility bill or online portal | |

| Average monthly electric bill ($) | Utility bill | |

| 12-month peak usage month | Utility bill history | |

| Roof age and material | Home inspection records | |

| Available roof space (sq ft) | Property records or aerial estimate |

Set your financing goals before you compare lenders

Once you know your usage, define what a good financing outcome looks like for your household. Decide on your maximum comfortable monthly payment and your preferred loan term, whether that is 10, 15, or 20 years. A shorter term means less total interest paid, but a higher monthly payment. A longer term lowers your monthly obligation but increases total interest over time.

Confirming your federal tax credit eligibility before accepting any offer matters just as much. If you owe at least $9,000 in federal taxes on a $30,000 system, you can apply the full 30% ITC in the year you install. If your tax liability is lower, you can carry the unused portion forward to the next tax year.

Knowing your tax liability before signing a loan helps you decide whether to use the credit to pay down principal early, which some solar loans are specifically structured to allow.

Step 2. Compare local financing options

Once you have your usage numbers and payment goals in hand, you’re ready to start searching for solar financing near me in a structured way. Most homeowners make the mistake of accepting the first financing offer their installer presents without checking what else is available. Shopping at least three to five lenders before committing gives you enough data to recognize a genuinely competitive rate and spot a weak offer quickly.

Where to look for local lenders

Your search for financing should cover four distinct source categories: your installer’s lending partners, local credit unions, regional banks, and state-backed programs. Each category has different approval criteria, rates, and benefits. Credit unions in Florida frequently offer solar loans at lower rates than national lenders because they operate as nonprofits and pass savings to members. Florida-based options like the PACE financing structure (Property Assessed Clean Energy) allow repayment through your property tax bill, which suits homeowners who want no separate monthly loan payment but are comfortable with a higher annual tax obligation.

PACE financing attaches to the property rather than to you personally, which means if you sell your home before the loan is repaid, the remaining balance transfers to the new owner.

Here is where to search within each category:

| Source Category | Examples | Best For |

|---|---|---|

| Installer lending partners | Mosaic, GoodLeap, Sunlight Financial | Convenience, solar-specific terms |

| Local credit unions | Florida-based credit unions | Lower rates, flexible approval |

| Regional banks | Community banks with green loan programs | Competitive HELOCs and personal loans |

| State and federal programs | PACE, FHA PowerSaver | Low-income eligibility, property-tied repayment |

How to compare offers side by side

Comparing loan offers on monthly payment alone will mislead you. Instead, request the full loan disclosure document from each lender and line up the following figures in a single spreadsheet: APR, total interest paid over the full term, any origination or dealer fees, and the prepayment penalty policy. Total cost of borrowing is the only number that tells you which offer actually saves you the most money over the life of the loan.

Step 3. Vet lenders and offers like a pro

Once you have multiple offers lined up, the next move is verifying that the lenders you’re considering are legitimate, licensed, and transparent about what they’re actually selling you. Finding solar financing near me through a quick online search can surface both reputable providers and predatory ones, often side by side. Spending 30 minutes vetting each lender before you sign anything can save you years of financial regret.

Verify lender credentials and licensing

Every lender offering consumer loans in Florida must hold a valid state license through the Office of Financial Regulation (OFR). You can confirm a lender’s status directly through the Florida OFR’s public license lookup portal. If a lender isn’t listed or their license shows as inactive, stop the conversation immediately. Also confirm whether the lender is a direct lender or a loan broker passing your application to a third party, since brokers add fees and reduce your negotiating leverage.

Ask each lender these four direct questions before moving forward:

- What is the APR and how is it calculated?

- Is there a dealer fee charged to my installer, and will it affect my system price?

- What is the prepayment penalty, if any?

- Does this loan report to credit bureaus, and what impact does it carry on my credit score?

Spot the warning signs in loan agreements

Loan agreements for solar financing can run 15 to 20 pages, and the language that costs you the most is buried in the middle. Look specifically for escalating interest clauses, which raise your rate after a promotional period ends, and dealer fee disclosures, which sometimes appear only in the fine print. A legitimate lender will give you a clear, itemized breakdown of the total loan cost without pressuring you to sign immediately.

If a lender pushes you to sign the same day you receive the offer, treat that as a serious warning sign and request at least 48 hours to review the documents carefully.

Your loan agreement should clearly state the total amount financed and total interest paid over the full term, along with any conditions under which your rate or terms can change. If any of those figures are missing or vague, ask for a revised disclosure before you proceed.

Step 4. Coordinate financing with your installer

Most homeowners treat financing and installation as two separate tracks, but they run parallel, and gaps in coordination between your lender and installer are one of the most common reasons solar projects stall or go over budget. Once you’ve settled on a lender, bring your installer into the conversation immediately. Your installer needs to know which lender you’re using, what documentation they require, and what the funding timeline looks like before they can schedule your installation with any certainty.

Get your installer and lender talking early

Your installer has likely worked with multiple solar lenders and understands the documentation each one typically requires. Ask your installer directly whether they have an existing relationship with your chosen lender, since a familiar lender relationship speeds up the approval and funding process significantly. If your lender is new to your installer, give both parties each other’s contact information and confirm they’ve connected before you sign the loan agreement.

Lender funding typically happens at project completion, not at signing, which means your installer needs to plan cash flow around that timeline before they commit to a start date.

Provide your installer with a copy of your loan approval letter and funding conditions so they know exactly what the lender needs to release funds. Some lenders require a signed completion certificate, a final inspection report, or utility interconnection approval before they wire payment to the installer.

Confirm the financing timeline before installation begins

Financing timelines vary by lender, and a mismatch between your loan funding date and your installation schedule can delay your project by weeks. Ask your lender for a clear written timeline covering approval, document review, and expected funding date. Then share that document with your installer so they can align your project start date accordingly.

Use this simple coordination checklist as a starting point:

| Coordination Step | Responsible Party | Deadline |

|---|---|---|

| Share loan approval letter with installer | You | Day of approval |

| Confirm lender funding conditions | Lender | Before signing |

| Submit completion documentation to lender | Installer | Day of final inspection |

| Confirm interconnection approval timeline | Installer | Before installation start |

Staying on top of this process means your search for solar financing near me converts into an actual installed system without unnecessary delays or surprises on either side.

Quick checklists and questions to ask

Keeping your research organized as you search for solar financing near me prevents small oversights from becoming costly mistakes. Use the checklists and question lists below as a practical reference at each stage of the process, from your first installer conversation to the moment you sign a loan agreement.

Before you accept any loan offer

Run through this checklist before committing to any financing offer. Each item represents a decision point that directly affects your total cost of borrowing or your eligibility for federal and state incentives.

- Confirmed your average monthly kWh usage from the last 12 months

- Calculated your estimated federal tax liability to size your ITC benefit correctly

- Requested loan disclosure documents from at least three lenders

- Compared total interest paid over the full term, not just monthly payment

- Confirmed no dealer fees are embedded in your system price

- Verified the lender’s license through the Florida Office of Financial Regulation

- Confirmed whether the loan is secured or unsecured and what collateral applies

- Reviewed the prepayment penalty clause in full

- Shared your loan approval letter and funding timeline with your installer

Skipping even one item on this list, particularly the dealer fee check, can cost you several thousand dollars over the life of your loan.

Questions to ask every lender

Before you sign anything, ask each lender these direct, specific questions and get the answers in writing. A lender who hedges or avoids answering clearly is a lender worth walking away from.

- What is the exact APR, and does it change at any point during the loan term?

- Is there a dealer fee charged to the installer, and how does it affect my total system cost?

- What is the total interest paid if I make only the minimum payments for the full term?

- Does this loan allow early payoff, and is there a prepayment penalty?

- How does this loan report to credit bureaus, and what is the impact on my credit profile?

- What documentation do you need from my installer before you release funds?

- What is your expected timeline from application approval to funding?

Next steps

You now have a complete framework for finding and evaluating solar financing near me, from pulling your utility usage numbers to coordinating your lender and installer before the first panel goes on your roof. The process works when you follow each step in order, compare at least three lenders on total cost rather than monthly payment, and verify every offer before you sign.

Your next move is straightforward. Get a quote from a licensed, experienced Florida installer who can give you an accurate system size, confirm your incentive eligibility, and walk you through financing options that fit your actual budget. Skipping that step leaves you comparing loan offers without knowing what you actually need to borrow.

Advance Solar & Spa has completed more than 50,000 installations across Florida and works with homeowners on both system design and financing guidance from day one. Request your free solar consultation and get the numbers you need to move forward with confidence.