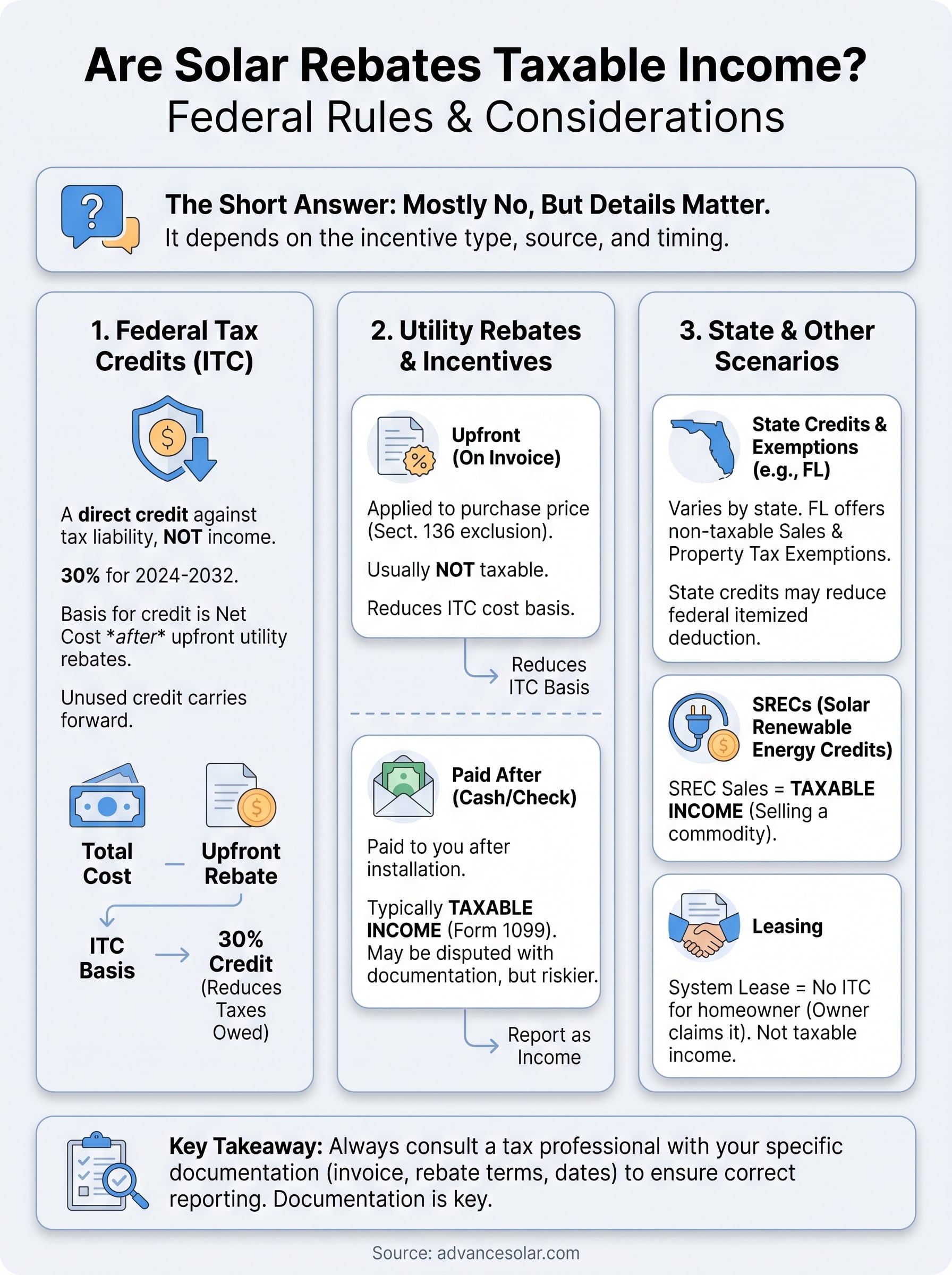

You installed solar panels, claimed some incentives, and now tax season has you second-guessing everything. The question, are solar rebates taxable income, comes up constantly, and the answer isn’t as straightforward as a simple yes or no. It depends on the type of incentive, where it came from, and how it interacts with your overall tax situation.

The short answer: most solar rebates and credits that homeowners receive do not count as taxable income. The federal Investment Tax Credit (ITC), for example, is a dollar-for-dollar reduction in tax liability, not income. Utility rebates, however, follow different rules, and misunderstanding the distinction can lead to errors on your return. Some incentives reduce your cost basis in the property, while others may trigger a reporting obligation you didn’t expect.

At Advance Solar & Spa, we’ve helped Florida homeowners and businesses navigate solar installations for over 40 years, more than 50,000 projects since 1983. Our certified solar consultants walk clients through not just the technical side of going solar, but also the financial picture, including how rebates and credits affect what you owe. While we’re not tax advisors, we’ve seen every type of incentive scenario play out across thousands of installations on both Florida coasts.

This article breaks down the federal rules around solar rebates and taxable income, covers the most common incentive types, and explains what homeowners actually need to report. If you’re claiming solar incentives, or planning to, this is the guide that helps you understand where the IRS draws the line.

Why solar rebate taxes confuse homeowners

Solar incentives come from multiple directions, federal programs, utility companies, and state governments, and each source follows a different set of tax rules. You might receive the federal Investment Tax Credit, a utility rebate, and a state credit all from a single solar installation, and the IRS treats each one differently. Most homeowners assume that because an incentive reduces the cost of solar panels, it either doesn’t count as income or always reduces what they owe in taxes. That assumption isn’t always correct, which is exactly why the question "are solar rebates taxable income" keeps coming up at tax time.

Three sources, three different rule sets

The federal government, state governments, and utility companies all offer solar incentives, but they operate under separate legal frameworks. A rebate from your utility company is typically governed by Section 136 of the Internal Revenue Code, which excludes certain energy conservation subsidies from gross income. The federal solar Investment Tax Credit falls under Section 25D of the tax code, which provides a direct credit against your tax liability rather than a reduction in income. State credits follow their own statutes, which vary by state and sometimes interact with federal rules in unexpected ways. When you stack multiple incentives on one project, you end up navigating overlapping rule sets that apply to the same installation but calculate the tax impact differently.

Confusion grows because many online summaries treat all solar incentives as one category. You’ll find articles that say solar incentives are "tax-free" without explaining that the category covers several distinct instruments. A rebate applied directly to your installation cost behaves differently from a rebate paid as a check after installation, and a state tax credit may or may not reduce your federal deduction depending on how you itemize. If you rely on a generalized answer without understanding which incentive you received and where it came from, you risk under-reporting income or, on the flip side, paying taxes on money you didn’t need to report.

Why the cost basis issue catches people off guard

Even homeowners who correctly identify their rebate as non-taxable can still miss a secondary tax consequence: the cost basis reduction. When a utility or energy provider gives you a rebate, the IRS often requires you to reduce the cost basis of your solar system by the rebate amount. This matters because your cost basis affects depreciation calculations for business installations and, in some scenarios, capital gains calculations if you sell your home after significant system upgrades. Most homeowners never think about cost basis when they install solar panels, so this rule catches them off guard, especially when they’re working with a tax preparer who isn’t familiar with energy incentive accounting.

The cost basis reduction rule is one of the most frequently overlooked consequences of receiving a utility solar rebate, and it can affect your taxes years after the original installation.

Another layer of confusion comes from timing. The federal ITC applies to the tax year you place your solar system in service, meaning the year installation is completed and the system is operational. Utility rebates, however, can arrive weeks or months after installation closes, sometimes crossing into a different tax year. That gap creates uncertainty: do you report the rebate in the year you installed the system or the year the funds arrived? The answer typically depends on when you received the money and whether the rebate was applied as a purchase price reduction upfront or paid to you afterward. Getting the timing wrong is one of the most common filing errors homeowners make when reporting solar incentives.

The main types of solar incentives and how they differ

Before you can answer whether are solar rebates taxable income applies to your situation, you need to know exactly what type of incentive you received. The word "rebate" gets used loosely, but solar incentives actually fall into three distinct categories, each with its own mechanics and tax treatment. Lumping them together is where most of the confusion starts.

Federal tax credits

The federal Residential Clean Energy Credit, commonly called the solar Investment Tax Credit (ITC), lets you claim a percentage of your total solar installation cost directly against your federal income tax liability. For systems placed in service in 2024 and 2025, that percentage is 30%. This credit reduces the tax you owe, dollar for dollar. It does not show up as income on your return, and it does not get added to your adjusted gross income. If the credit exceeds your tax liability for the year, the unused portion carries forward to the next tax year.

A tax credit is not the same as a tax deduction. A credit reduces what you owe directly, while a deduction only reduces the income on which your tax is calculated.

Utility rebates

Utility rebates come from your electricity provider, not the government. Your utility company pays you a set amount for installing solar, usually calculated per watt of capacity or as a flat dollar figure. These payments can arrive as a check, a direct deposit, or as a reduction applied to your installation invoice before you pay the final bill. The source and delivery method of a utility rebate both matter when it comes to federal tax treatment, which is why this category gets its own rules under the tax code and requires separate analysis from any credits you claim.

State tax credits and grants

State-level programs vary widely. Some states offer a direct tax credit against your state income tax, similar in structure to the federal ITC but calculated at the state level. Others provide grants, which are upfront cash payments that require no repayment. Still others offer property tax exemptions on the added value solar panels bring to your home, or sales tax exemptions on the equipment purchase itself. Each of these instruments works differently:

| Incentive Type | How It Reduces Your Cost | Paid By |

|---|---|---|

| Federal ITC | Reduces federal tax owed | Federal government |

| Utility rebate | Reduces purchase price or paid after installation | Utility company |

| State tax credit | Reduces state tax owed | State government |

| State grant | Direct cash payment | State government |

| Property tax exemption | Reduces annual property tax bill | Local/state government |

Knowing which category your incentive falls into is the first step toward filing your return correctly.

When a solar rebate counts as taxable income federally

Not every solar incentive escapes federal taxation, and understanding when a rebate becomes reportable income is critical before you file. The IRS distinguishes between incentives that reduce your purchase price and incentives that put money directly in your pocket after the fact. That distinction determines whether the payment lands on your tax return as income.

Utility rebates paid to you after installation

When your utility company sends you a check or direct deposit after you’ve already paid the full cost of your solar system, the IRS typically treats that payment as ordinary income you must report. The exclusion under Section 136 of the Internal Revenue Code applies to subsidies that reduce your energy costs or offset the cost of purchasing or installing a solar system, but it carries specific conditions. If the rebate arrives after the transaction closes and is structured as a cash payment rather than a purchase price reduction, it may fall outside that exclusion entirely.

The timing and structure of a utility rebate, not just the source, determines whether the IRS considers it excludable from your gross income.

The form your rebate takes also affects how you report it. Some utility programs issue IRS Form 1099-MISC or a similar document when they pay rebates above a certain dollar threshold, which signals that the payer has already reported the amount to the IRS. If you receive a 1099 for a solar rebate, you need to include that amount in your gross income on your federal return, even if you believe it should be excluded. Working with your tax advisor to document the exclusion position is essential if you choose to challenge that reporting.

Business and commercial installations

If you installed solar panels on a commercial property or as part of a business, the rules around taxable income shift further. Business installations use the federal Investment Tax Credit under Section 48 of the Internal Revenue Code, not the residential Section 25D credit. Under the commercial rules, rebates or grants you receive reduce your depreciable basis in the system, which changes your depreciation deductions over time. In some cases, portions of grants or incentives received by businesses are reportable as income if they exceed specific thresholds or don’t meet program requirements for exclusion.

Many Florida business owners ask are solar rebates taxable income when they combine a utility rebate with the commercial ITC, and the answer depends on whether the rebate reduces the depreciable basis or gets treated as a separate taxable receipt. Keeping documentation that clearly shows how each incentive was structured and applied protects your position if the IRS reviews your return.

When a solar rebate usually is not taxable income

Most homeowners asking are solar rebates taxable income will find that the majority of common solar incentives do not require you to report anything extra. The key factors are who issued the incentive, how it was delivered, and what the tax code says about that specific type of payment. When those factors line up correctly, your incentive reduces what you pay for solar without adding to your federal taxable income.

Utility rebates applied directly to your installation cost

When your utility company reduces your purchase price upfront, before you pay the final bill, that rebate generally falls under the Section 136 exclusion in the Internal Revenue Code. Section 136 specifically excludes from gross income any subsidy provided by a public utility for the purchase or installation of an energy conservation measure. Solar panels installed on your primary residence qualify under this exclusion in most cases, which means you do not report the rebate as income on your federal return.

The Section 136 exclusion applies when the rebate reduces your cost at the time of purchase, not when it arrives as a separate cash payment afterward.

Even under this exclusion, you still need to reduce your cost basis in the system by the rebate amount. That step does not affect your taxes in the year of installation, but it matters if you sell the property later or if depreciation becomes relevant in a business context.

The federal Investment Tax Credit

The federal Residential Clean Energy Credit is never taxable income because it is not income at all. It reduces the federal income tax you already owe, dollar for dollar. You claim it on IRS Form 5695, and the credit applies directly against your tax liability for the year your system was placed in service. No additional income gets added to your return, and no reporting obligation applies beyond filing that form correctly.

State tax credits and property tax exemptions

State solar tax credits work the same way as the federal ITC from an income perspective: they reduce your state tax liability rather than adding to your income. Florida does not have a state income tax, so this applies more directly to homeowners in other states, but the principle holds broadly. Florida homeowners do benefit from the state’s solar equipment sales tax exemption and the property tax exclusion for added home value from solar installations, neither of which creates a taxable event. These exemptions simply lower your purchase cost or annual tax bill without triggering any income reporting requirement at the federal or state level.

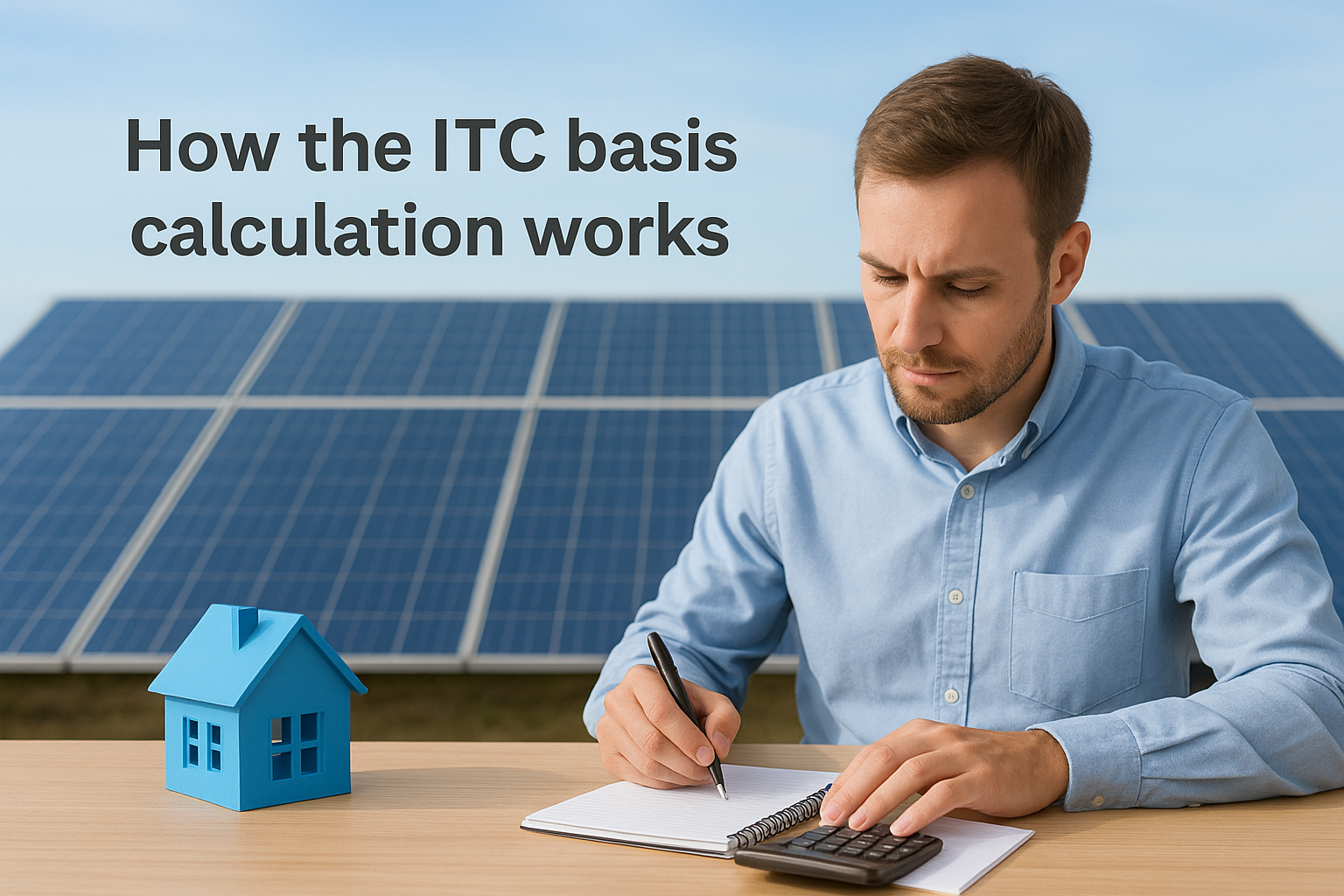

How rebates change your federal solar tax credit

Understanding are solar rebates taxable income is only part of the picture. Even when a rebate doesn’t trigger a tax bill, it can still reduce the dollar amount of your federal solar tax credit. That reduction happens quietly, through a calculation most homeowners don’t notice until they sit down with a tax preparer and realize their credit came in lower than expected.

How the ITC basis calculation works

The federal Residential Clean Energy Credit equals 30% of your eligible installation costs, but the key word is "eligible." The IRS calculates your credit based on your net cost after certain rebates are applied, not your total invoice before incentives. When a utility company reduces your purchase price upfront, that rebate lowers the amount you actually paid for the system, and the IRS uses that lower figure as your tax credit basis.

Here’s a straightforward example: if your solar installation costs $20,000 and your utility applies a $2,000 rebate directly to your invoice, you pay $18,000 out of pocket. Your ITC is then 30% of $18,000, which equals $5,400, not the $6,000 you would have received on the full amount. That $600 difference is real money, and missing it in your calculation means you either under-claim the credit or have to amend your return later.

When a utility rebate reduces your purchase price at the time of sale, it also reduces the cost basis the IRS uses to calculate your 30% federal solar tax credit.

The math changes if the rebate arrives as a separate payment after you’ve already paid the full installation invoice. In that scenario, you paid the full $20,000, so your ITC basis is $20,000 and your credit is $6,000. The rebate check you receive afterward may carry its own tax consequences as discussed earlier, but it does not retroactively shrink your credit calculation because it wasn’t applied to the purchase price at closing.

What to do if your rebate and installation cross tax years

Sometimes a utility rebate gets approved in one tax year but paid in the next. This gap matters because your ITC is claimed in the year your system is placed in service, which is the year installation is complete and the system is operational. If your rebate hadn’t arrived yet when you filed, and you correctly based your ITC on your full net out-of-pocket cost, you should be in good shape. However, if the rebate later reduces your basis retroactively under program terms, you may need to file an amended return to correct your credit amount. Keeping documentation of when each payment occurred and how your installer structured the transaction protects you in either situation.

How to report solar rebates and credits on your return

Knowing are solar rebates taxable income only helps you if you also know where to put the numbers on your actual return. The IRS requires specific forms for solar incentives, and using the wrong form or leaving a line blank can trigger a review or delay your refund. Getting the paperwork right the first time saves you from amending later.

Claiming the federal ITC on Form 5695

You report the Residential Clean Energy Credit on IRS Form 5695, Part I. This form walks you through the calculation step by step, starting with your total eligible costs for the solar system and ending with the credit amount you carry to Schedule 3 and then to your Form 1040. The year you place your system in service is the year you file this form, even if you haven’t paid the full balance yet.

If your credit exceeds your tax liability for the year, the unused amount carries forward automatically to the next tax year, so you do not lose the benefit.

Follow these steps when completing Form 5695:

- Enter the total cost of your solar electric system on line 1, using your net amount after any upfront utility rebates reduced your purchase price.

- Add any other qualifying clean energy costs, such as battery storage or solar water heating, on the relevant lines.

- Multiply the total by 30% to get your credit amount on line 6.

- Transfer the final credit to Schedule 3, Line 5, and from there to your Form 1040.

Reporting utility rebates received as cash

If your utility company sent you a check or direct deposit after your installation closed, and the payment came with a Form 1099-MISC or 1099-G, you need to report that amount as income. Enter it on Schedule 1 of your Form 1040, under "Other Income," and label it clearly as a utility solar rebate so the source is obvious to anyone reviewing your return.

You can take an exclusion position under Section 136 if you believe the payment qualifies as a non-taxable energy conservation subsidy, but document your reasoning thoroughly. Attach a written statement explaining the basis for the exclusion, referencing the specific program terms and the IRS code section you’re relying on. Your tax preparer can help you structure that argument correctly. If you skip the documentation and the IRS disagrees with your position, the penalty and interest exposure is far larger than simply reporting the income in the first place.

State tax rules and what to check where you live

Federal rules give you a solid framework, but state tax treatment of solar incentives varies significantly from one state to the next. When you ask are solar rebates taxable income, the federal answer covers only part of your actual tax picture. Several states have their own income taxes, their own solar credit programs, and their own rules about whether those credits interact with your federal return. Checking your state’s specific rules before you file prevents surprises that could require an amended return down the road.

Florida homeowners: what the state covers

Florida gives solar owners two meaningful financial protections that reduce costs without triggering any income reporting obligation. First, the state exempts solar energy equipment from sales tax at the point of purchase, which means you don’t pay Florida’s standard sales tax rate on your panels, inverters, or related components. Second, Florida law excludes the added property value from solar installations when calculating your annual property tax assessment, so your property taxes won’t increase simply because you added solar to your home. Neither exemption creates a taxable event, and neither shows up anywhere on a tax return.

Because Florida has no state income tax, you also don’t need to worry about a separate state solar tax credit return or state-level credit carryforward rules. Your tax preparation for Florida-based solar incentives focuses entirely on federal forms. That simplifies the process considerably compared to what homeowners in states like California, New York, or Massachusetts deal with when they stack state credits on top of federal ones.

What homeowners in other states need to verify

If you live in a state with an income tax and a state-level solar tax credit, you need to check whether that credit reduces your federal deduction in any way. In states where you itemize and deduct state income taxes paid, receiving a state solar credit can lower your state tax bill, which in turn reduces the state tax deduction you take on your federal Schedule A. That interaction can affect your federal taxes indirectly, even though the state credit itself isn’t income.

A state solar tax credit that lowers your state tax bill can reduce your federal itemized deduction for state taxes paid, which creates a secondary federal tax effect worth calculating before you file.

You should also confirm whether your state treats utility rebates differently from state credits, since some states follow the federal Section 136 exclusion and others apply their own rules. Check your state’s department of revenue website directly for guidance, or ask a tax professional who handles energy incentive filings in your specific state. Getting a clear answer for your location takes far less time than correcting an error after the IRS or your state agency flags a discrepancy.

Common edge cases and quick answers

Some situations don’t fit neatly into the standard rules, and that’s where homeowners most often make mistakes. The question of are solar rebates taxable income gets more complicated when your installation involves a lease, a credit that crosses tax years, or a payment type you haven’t encountered before. The following edge cases cover the scenarios that come up most frequently and give you a direct answer for each.

What happens if you lease your solar panels?

If you lease your solar system rather than own it, you do not claim the federal ITC because you don’t own the equipment. The leasing company owns the system, takes the tax credit, and typically passes some of the savings to you through a lower monthly lease payment. Any reduction in your electricity bill from that arrangement is not reportable income, and you won’t receive any rebates directly tied to the installation. Your tax situation stays simple because you have no ownership stake and therefore no credit to claim or rebate to track.

What if your rebate check arrives the year after your installation?

You claim the federal ITC in the tax year your system is placed in service, regardless of when a rebate check arrives. If your utility sends a rebate in January of the following year, that payment stands on its own timeline. Your ITC calculation uses your net cost at the time of installation, not the rebate received later. The subsequent check may carry its own income reporting obligation depending on how the utility structured the program.

If your installation and your rebate fall in different tax years, keep both documents separate and treat each one according to the rules for the year it occurred.

What about Solar Renewable Energy Credits?

SRECs, or Solar Renewable Energy Credits, are different from standard rebates. When your solar system generates electricity, it also produces SRECs that you can sell to utility companies trying to meet state renewable portfolio standards. The IRS treats SREC sales as taxable income because you’re selling a commodity, not receiving a subsidy for installing a system. You report SREC proceeds as ordinary income on Schedule 1 of your Form 1040, and you’ll owe federal income tax on the full amount you received.

What if your tax credit exceeds your tax liability?

The unused federal ITC carries forward to the following tax year automatically. You don’t lose the benefit if your liability is too low to absorb the entire credit in year one. Carry the remaining credit forward on Form 5695 in the next filing year and apply it until it’s fully used. There is no limit on how many years you can carry it forward under current law.

A simple next step before you file

The question are solar rebates taxable income has a nuanced answer that depends on the type of incentive, how it was delivered, and when you received it. Most homeowners walk away with no additional taxable income from their solar installation, but the details matter enough to verify before you file.

Before you submit your return, gather your installation invoice, any rebate documentation from your utility, and your system’s placed-in-service date. Hand those documents to a tax professional who has experience with energy incentive filings, and ask them to confirm your cost basis, your ITC calculation, and whether any payments require reporting.

If you’re still in the planning stage, talking to a solar consultant first puts you in a much stronger position. The team at Advance Solar & Spa has guided Florida homeowners through more than 50,000 installations and can walk you through the full financial picture before you commit.