A pool heat pump keeps your water comfortable year-round, but the upfront cost, typically $3,000 to $7,000 installed, can give homeowners pause. That’s where pool heat pump financing comes in. With the right payment plan, you can start enjoying a warm pool now and spread the cost over manageable monthly installments instead of draining your savings all at once.

But financing options vary widely. Some dealers offer zero-interest promotional periods, others work with third-party lenders, and a few programs come with terms that aren’t exactly in your favor. Knowing what’s available and what to watch out for makes a real difference in how much you ultimately pay.

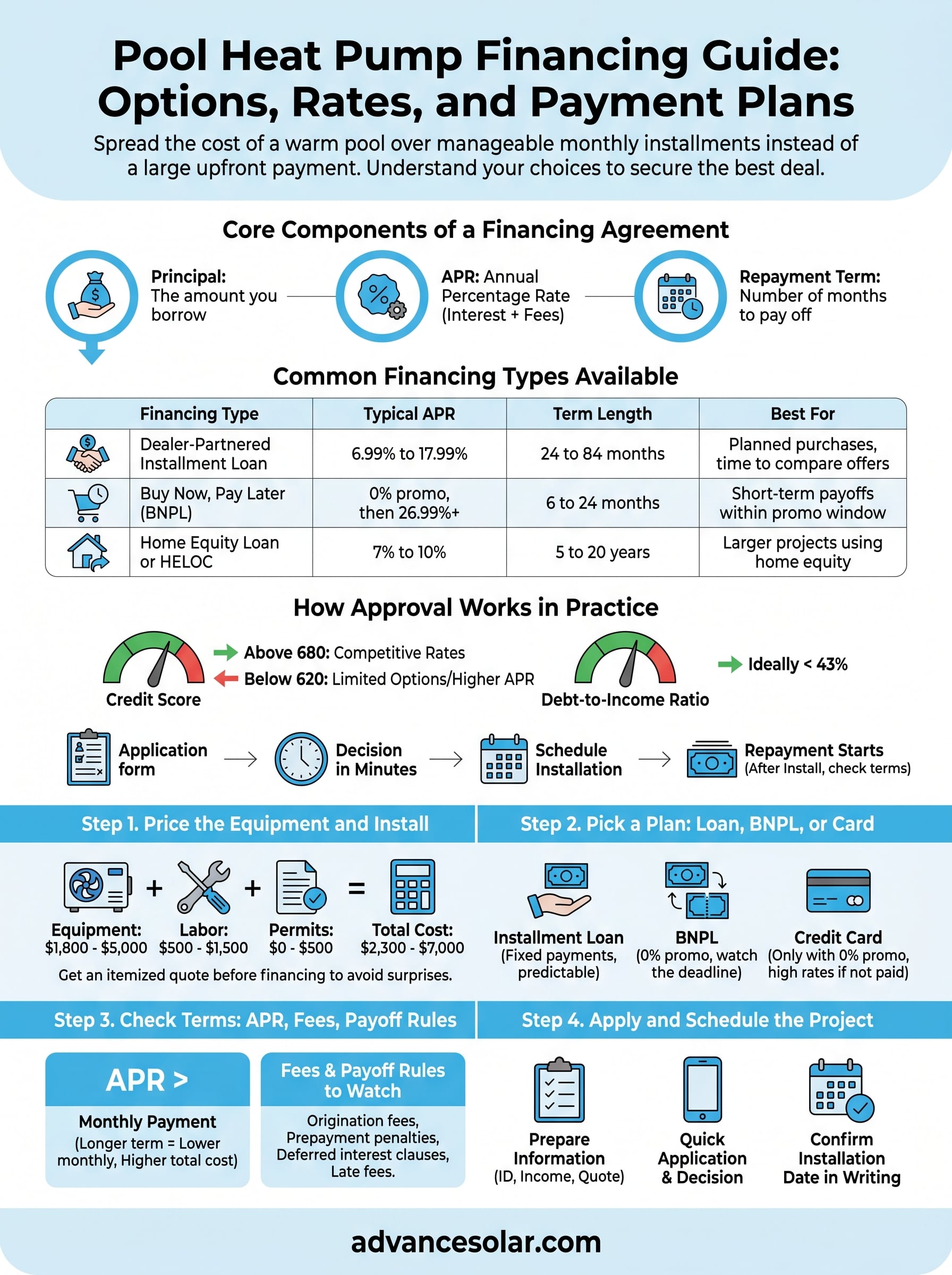

At Advance Solar & Spa, we’ve been installing pool heating systems across Florida since 1983, more than 50,000 installations and counting. Our team helps homeowners find equipment and financing that fits their budget. In this guide, we’ll walk you through the main financing options, typical rates, what affects your approval, and how to choose a payment plan that actually works for your situation.

How Pool Heat Pump Financing Works

Pool heat pump financing works like most home improvement loans: a lender, dealer, or credit company covers your upfront cost, and you repay the amount in fixed monthly installments over an agreed term. The key difference from a general personal loan is that many pool equipment dealers have already partnered with specific financing companies, so you can often apply directly at the point of sale rather than hunting down a lender on your own before the project starts.

The shorter your repayment term, the less interest you pay overall, even if the monthly payments run higher.

What the financing structure looks like

Most pool heat pump financing agreements share three core components: the principal (the amount you borrow), the APR (annual percentage rate, which includes both interest and fees), and the repayment term (the number of months you have to pay it off). Some agreements also include a deferred interest clause, which means if you don’t pay off the full balance before a promotional period ends, interest charges from that entire period get added back to your balance in one shot.

Here’s a quick breakdown of the three most common financing types available:

| Financing Type | Typical APR | Term Length | Best For |

|---|---|---|---|

| Dealer-partnered installment loan | 6.99% to 17.99% | 24 to 84 months | Planned purchases with time to compare |

| Buy Now, Pay Later (BNPL) | 0% promo, then 26.99%+ | 6 to 24 months | Short-term payoffs within the promo window |

| Home equity loan or HELOC | 7% to 10% | 5 to 20 years | Larger projects where homeowners carry equity |

How approval works in practice

Lenders primarily evaluate your credit score and debt-to-income ratio when you apply. A credit score above 680 typically qualifies you for competitive rates, while scores below 620 may limit your options or push your APR noticeably higher. Your debt-to-income ratio should ideally stay below 43%, which is a standard threshold used by most consumer lenders.

For dealer-arranged financing, you’ll usually receive a decision within minutes, and same-day approval is common. Once approved, the lender pays the contractor or dealer directly, and your repayment schedule typically starts after installation is complete, though some agreements begin the clock on the approval date, so confirm that detail before you sign.

Step 1. Price the Equipment and Install

Before you explore any pool heat pump financing plan, you need a firm number to finance. Guessing at the cost or working from a rough estimate leads to under-borrowing and out-of-pocket surprises after installation begins. Your total project cost drives everything: the loan amount you request, the term you choose, and the monthly payment you’ll be managing.

What Goes Into the Total Cost

Your invoice will include more than just the unit itself. A standard pool heat pump installation typically breaks down into three cost categories: the equipment, the labor, and permit fees if your municipality requires them.

| Cost Category | Typical Range |

|---|---|

| Pool heat pump unit | $1,800 to $5,000 |

| Installation labor | $500 to $1,500 |

| Permits and inspections | $0 to $500 |

| Total project cost | $2,300 to $7,000 |

Getting a written, itemized quote before you apply for financing protects you from cost overruns that could leave your loan short of the final bill.

How to Request a Useful Quote

Contact at least two or three installers and ask for a line-item quote that separates equipment costs from labor. When you call or email, use this simple request template:

"Please provide a written quote listing the heat pump model and price, labor costs, any permit fees, and the estimated installation timeline."

This approach gives you a clear, comparable number to bring into the financing conversation, and it prevents installers from bundling costs in ways that make offers difficult to compare side by side.

Step 2. Pick a Plan: Loan, BNPL, or Card

With your total project cost in hand, you can now match it to the right financing structure. Each option suits a different financial situation, so the best choice depends on your credit profile, how quickly you can repay, and whether your dealer offers a specific program.

Installment Loan

A dealer-arranged installment loan is the most common route for pool heat pump financing. You borrow a fixed amount, receive a set monthly payment, and pay it off over a term that typically runs 24 to 84 months. This option works well if you want predictable payments and a clear payoff date.

If your credit score sits above 680, you’ll likely qualify for the lower end of the APR range, which can save you hundreds over the life of the loan.

Buy Now, Pay Later

BNPL plans let you split your purchase into smaller installments, often with a zero-percent promotional period ranging from 6 to 24 months. The critical rule here: pay off the full balance before the promo period ends, or you’ll owe backdated interest on the original amount. Ask your dealer which BNPL providers they work with, as approval is typically instant at checkout.

Credit Card

Using a credit card makes sense only if you have access to a 0% APR promotional offer and can realistically pay off the balance within that window. Standard credit card rates run 20% or higher, which turns a manageable project into an expensive one fast. Reserve this option for smaller balances you can clear in three to six months.

Step 3. Check Terms: APR, Fees, Payoff Rules

Once you’ve picked a financing structure, slow down before you sign. The advertised monthly payment rarely tells the full story. Reading the actual loan agreement takes about ten minutes and can save you a significant amount over the life of your pool heat pump financing plan.

APR: What the Number Actually Means

APR combines the interest rate and any lender fees into a single annualized percentage, so it gives you a more accurate picture of total borrowing cost than the interest rate alone. When comparing offers, always compare APRs, not just monthly payments, because a longer term lowers your monthly payment while quietly increasing what you pay overall.

A $5,000 loan at 9.99% APR over 60 months costs roughly $1,374 in interest. The same loan at 17.99% APR costs about $2,693.

Fees and Payoff Rules to Watch

Some lenders charge fees that don’t show up in the APR calculation, and deferred interest clauses can cost you hundreds if you miss the payoff window. Before you sign, confirm each of these items directly with your lender:

| Term to Verify | What to Ask |

|---|---|

| Origination fee | Is there a fee charged when the loan is issued? |

| Prepayment penalty | Can you pay off early without a fee? |

| Deferred interest clause | Does unpaid balance trigger backdated interest? |

| First payment date | Does repayment start at approval or after installation? |

| Late payment fee | What is the penalty and grace period? |

Ask for these answers in writing before you commit. If a lender won’t provide clear written answers, treat that as a reason to look at another offer.

Step 4. Apply and Schedule the Project

Once you’ve reviewed the terms and chosen your financing plan, the actual application process moves quickly. Most dealer-arranged lenders run a soft credit pull first, which won’t affect your credit score, and then a hard pull only when you formally accept an offer. Have your basic financial information ready before you start so you’re not hunting for documents mid-application.

What to Prepare Before You Apply

Gather these details in advance to avoid delays on your pool heat pump financing application:

- Full legal name, address, and Social Security number

- Annual income and current employer information

- Monthly housing payment (rent or mortgage)

- The itemized project quote from your installer

Most online applications take under five minutes to complete. Once you submit, lenders typically deliver a decision within seconds to a few minutes. If your application requires additional income verification, expect a follow-up request within one business day.

Applying with your installer present, whether in person or on a call, means any questions about the project scope get answered immediately rather than slowing down your approval.

Schedule Installation Right After Approval

Don’t wait once you receive approval. Popular installation windows fill up quickly, especially during peak pool season in Florida. Contact your installer the same day you’re approved and confirm the project start date in writing. Use this simple confirmation message:

"I’ve been approved for financing. Please confirm the installation date, the equipment model being installed, and the total amount that will be invoiced to the lender."

Getting that confirmation in writing protects both parties and keeps your project timeline on track from day one.

Next Steps

You now have everything you need to move forward with pool heat pump financing confidently. Start by getting two or three itemized quotes from licensed installers so you know your exact project cost before you apply for anything. Then match that number to the financing structure that fits your credit profile and repayment timeline. If a dealer offers a BNPL plan, confirm the promotional period length and make sure you can clear the balance before it expires. If you’re leaning toward an installment loan, compare APRs across at least two offers before you commit.

Once you pick a plan, verify the key terms in writing and schedule installation the same day you’re approved. Waiting costs you nothing except a warmer pool sooner. If you’re in Florida and want to talk through your options with a team that has handled more than 50,000 installations, contact Advance Solar & Spa and get a free quote today.