The federal solar tax credit can knock thousands of dollars off a solar installation, but only if you qualify and know how the federal solar tax credit works before you file. With the Investment Tax Credit still available at 30% through 2032 thanks to the Inflation Reduction Act, Florida homeowners have one of the strongest financial incentives in the country to go solar right now.

At Advance Solar & Spa, we’ve handled over 50,000 installations since 1983, and the tax credit comes up in nearly every consultation we run across Fort Myers, Naples, Fort Lauderdale, and Sarasota. The same questions keep surfacing: Is the credit a refund or a reduction in what I owe? What expenses actually qualify? What happens if my tax liability is lower than the credit amount? These are critical details, and getting them wrong can mean leaving real money on the table.

This article answers all of it. We’ll cover eligibility requirements, the exact percentage of costs the credit covers, how it differs from a tax deduction, and how the carryforward provision works if you can’t use the full credit in one year. No tax jargon, no guesswork, just a clear breakdown built from four decades of helping Floridians make smart solar investments.

Why the federal solar tax credit matters

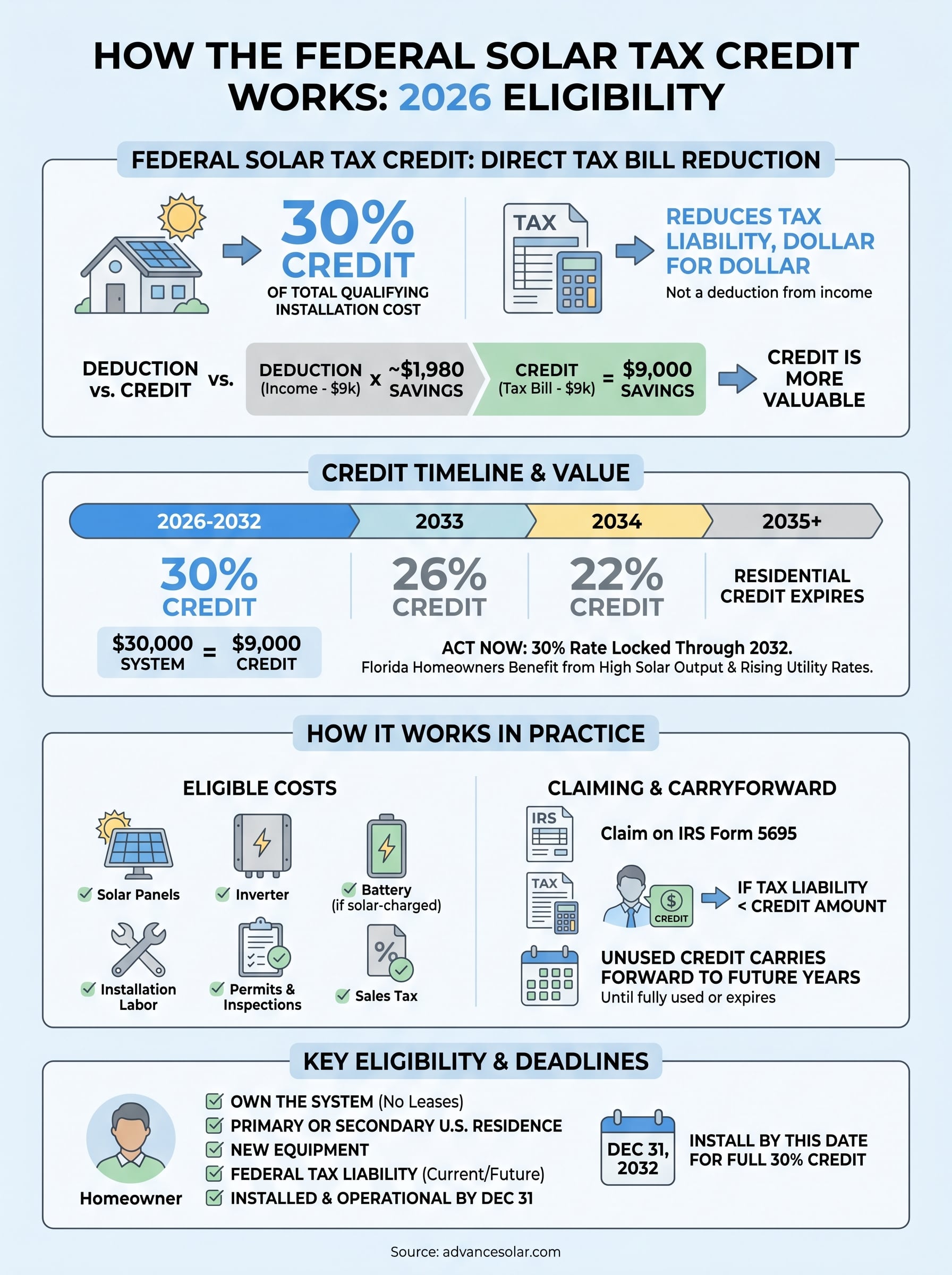

The federal solar tax credit is one of the most valuable financial tools available to homeowners right now. At 30% of your total installation cost, the credit directly reduces your federal tax bill dollar for dollar, not just the taxable income you report. For a typical Florida solar installation that runs between $25,000 and $35,000, that translates to a credit worth $7,500 to $10,500 coming straight off your tax liability. That kind of reduction changes the return on investment calculation significantly compared to purchasing solar without any incentive in place.

A 30% credit on a $30,000 solar installation removes $9,000 from your federal tax bill, not just from your taxable income.

The difference between a tax credit and a tax deduction

Many homeowners confuse tax credits with tax deductions, and that confusion can lead to seriously underestimating how powerful this incentive is. A tax deduction lowers the amount of income the IRS taxes you on. A tax credit lowers your actual tax bill. If you owe $12,000 in federal taxes and you hold a $9,000 credit, your liability drops to $3,000. A deduction of that same $9,000 at a 22% marginal rate would only reduce your bill by roughly $1,980.

That gap is significant. Grasping this distinction is central to understanding how the federal solar tax credit works in practice, and why homeowners who run the numbers often find it more impactful than they expected. The credit doesn’t soften your tax bill around the edges; it cuts directly into your liability and keeps more cash in your hands at tax time.

Why timing this credit correctly matters for Florida homeowners

Florida homeowners are in a particularly strong position to take advantage of this incentive because electricity rates in the state have risen steadily over the past decade, and Florida ranks among the top states for solar energy production due to its high solar irradiance levels. The combination of elevated utility costs and strong sun output means your system starts generating real financial returns quickly, and the federal credit compresses your payback period even further.

The credit holds at 30% through 2032, then steps down to 26% in 2033 and 22% in 2034 before expiring entirely for residential installations in 2035 unless Congress acts to extend it. That schedule matters more than most homeowners realize. Waiting past 2032 on the same installation at the same price could cost you thousands of dollars in lost credit value with no change to any other part of your situation.

Florida homeowners also operate without a state income tax, which means the federal credit carries all the weight on the tax side when you go solar here. You won’t layer additional state tax credits on top of it, so capturing the full federal credit in the year you install is the single most important financial move you can make. Getting your system in the ground and claiming the credit correctly is where the real financial leverage lives for Florida residents.

How the credit reduces your taxes

Understanding how the federal solar tax credit works starts with the mechanics of what happens at the IRS level when you file. The credit is applied directly against your calculated federal income tax liability, the final number you owe after deductions and other adjustments have already been factored in. If your tax software or accountant arrives at a figure you owe before the credit, the IRS subtracts the credit from that number, and you only pay what remains.

The math behind a 30% credit

Your credit equals 30% of every eligible dollar you spend on your solar installation. That includes equipment, labor, and several other qualifying costs covered in a later section. The table below shows what the credit looks like at different system price points to give you a concrete sense of the reduction you’re working with.

| System Cost | 30% Credit | Out-of-Pocket After Credit |

|---|---|---|

| $20,000 | $6,000 | $14,000 |

| $25,000 | $7,500 | $17,500 |

| $30,000 | $9,000 | $21,000 |

| $35,000 | $10,500 | $24,500 |

| $40,000 | $12,000 | $28,000 |

The credit cuts your tax bill dollar for dollar, so a $9,000 credit on a $30,000 system removes $9,000 from what you owe, not just from your taxable income.

Run your real installation estimate through that 30% figure and you’ll see quickly why this credit changes the financial case for solar more than most homeowners expect.

Carrying the credit forward

The IRS limits how much credit you can apply in a single year to your actual tax liability for that year. You cannot use more credit than you owe. If your credit exceeds your liability, you do not lose the remainder. The IRS allows you to carry the unused portion forward to the next tax year and apply it against that year’s liability instead.

That carryforward provision has no complicated application process. You simply report the unused amount on your return for the following year using the same IRS Form 5695. The credit follows your liability until it is fully used. For most Florida homeowners with standard income levels, the credit clears within one to two tax years without any portion going to waste.

Who qualifies in 2026 and key deadlines

The IRS sets clear eligibility criteria for the residential clean energy credit, and most Florida homeowners who install solar in 2026 will meet them without issue. The credit applies to primary and secondary residences located in the United States, so a vacation home in Naples qualifies the same as your main residence in Fort Myers. You do not need to own a business or hold any special tax status to claim it.

Core eligibility requirements

Understanding how the federal solar tax credit works from an eligibility standpoint comes down to a handful of conditions the IRS expects you to meet before you file. You must own the solar system outright, meaning leased systems or power purchase agreements do not qualify since the leasing company, not you, claims the credit in those arrangements. You must also have a federal tax liability in the year you claim the credit, or carry the unused portion forward to a year when you do. The system must be new or being used for the first time, and it must be installed at a U.S. residence you own.

If you lease your solar system instead of buying it outright, the leasing company keeps the tax credit, not you.

Here is a quick reference list of the main eligibility conditions:

- You own the solar system, not leasing it

- The system is installed at a U.S. residence you own

- The equipment is new or placed in service for the first time

- You have federal income tax liability in the claim year or a future carryforward year

- The system is fully installed and operational by December 31 of the tax year you are claiming

The 2032 deadline and what comes after

The credit currently holds at 30% through December 31, 2032 under the Inflation Reduction Act. Any system installed and placed in service by that date locks in the full 30% rate. After 2032, the percentage steps down to 26% in 2033, then drops again to 22% in 2034 before the residential credit expires entirely in 2035 unless Congress acts to renew it.

For 2026, you have plenty of runway to plan carefully, gather quotes, and complete an installation without pressure. The 30% rate remains fixed for six more years, but solar permitting and utility interconnection timelines in Florida can stretch across several months. Starting your process early in the calendar year keeps you comfortably clear of any deadline risk and gives your installer room to handle any delays without rushing the job.

What costs count toward the credit

The IRS definition of eligible costs for the residential clean energy credit is broader than most homeowners expect. Understanding how the federal solar tax credit works on the cost side means you capture the full credit amount rather than undershooting it by leaving out qualifying expenses. Your 30% credit applies to the entire project cost, not just the panels themselves, so getting an accurate total before you file matters significantly.

Equipment and installation labor

The core of your eligible costs sits in the hardware and labor that make your system functional. Solar panels, inverters, mounting systems, and the electrical wiring connecting everything together all count toward your qualifying total. If you add a battery storage system like a Tesla Powerwall or Enphase IQ Battery as part of the same installation, the battery cost qualifies as well. The IRS requires the battery to be charged primarily by your solar panels to qualify, but systems installed by certified professionals are typically configured to meet that standard automatically.

Battery storage costs are fully eligible when the battery is charged primarily by your solar installation, which is standard in professionally designed systems.

Labor costs for the actual installation are fully included in your eligible total. Every hour your installation crew spends mounting panels, running conduit, configuring your inverter, or completing the electrical hookup adds to the number you multiply by 30%. This is a meaningful addition since labor regularly represents 10% to 20% of a total project cost in Florida.

Permit fees, inspections, and sales tax

Your project costs extend beyond the equipment and the crew installing it. Permit fees required by your local municipality count toward the credit. Electrical inspection fees tied to the solar installation count as well. If your county requires a structural assessment before approving a rooftop installation, that inspection fee is included. Sales tax paid on any qualifying equipment or materials is part of your eligible total too, which adds up on a system priced at $30,000 or more.

What does not qualify is equally important to know. Roof repairs or replacements needed before installation do not count unless the roofing material itself is a solar product, such as solar roof tiles. Standard grid interconnection fees paid to your utility are also excluded from the qualifying total.

How to claim it on your tax return

Claiming the credit does not require a complicated filing process, but it does require one specific form that many first-time solar owners overlook. Understanding how the federal solar tax credit works at the filing stage means your credit gets applied correctly and you do not miss out on a dollar you have already earned by completing your installation. The process runs through your standard federal income tax return, whether you file with software or through a tax professional.

IRS Form 5695: The only form you need

The entire residential clean energy credit flows through IRS Form 5695, a single-page form titled "Residential Energy Credits." You enter your total qualifying costs on the form, the IRS calculates 30% of that figure automatically, and the resulting credit transfers directly to your Form 1040 as a reduction against your tax liability. If you use tax preparation software, the program walks you through a short interview and populates Form 5695 for you based on your answers.

Keep every receipt, invoice, and contract from your solar installation in one place before you file. You will not attach them to your return, but the IRS may request them if your return is ever audited.

Before you file, gather the following documents so you have accurate numbers ready:

- Final invoice from your installer showing the complete project cost

- Permit fees and inspection receipts paid during the installation process

- Sales tax records for equipment and materials if itemized separately

- Battery storage documentation if you added backup storage to your system

Working with a tax professional

Filing Form 5695 is straightforward enough that most tax software handles it without friction, but working with a CPA or enrolled agent who has experience with energy credits adds a layer of accuracy that pays off on larger systems. A qualified tax professional confirms that your eligible cost total is complete, catches any deductible expenses you might have missed, and handles the carryforward calculation correctly if your credit exceeds your liability for the year.

Your installer should provide documentation that clearly separates equipment costs, labor, and permit fees in the final invoice. Bring that breakdown directly to your tax preparer so the credit is calculated from the full qualifying amount rather than an estimate.

If your tax liability is too low

Not everyone owes enough in federal taxes to absorb a large solar credit in a single year. If your tax liability falls below your credit amount, you will not lose the difference. Understanding how the federal solar tax credit works in this specific scenario is just as important as knowing the credit percentage, because the carryforward provision is what makes the credit usable for homeowners across a range of income levels.

How the carryforward provision works in practice

The IRS allows you to carry any unused credit balance forward to the following tax year and apply it against that year’s liability. You report the leftover amount on Form 5695 when you file the next year’s return, and the credit reduces your liability again until it’s fully consumed. There is no penalty for using the carryforward, and no separate application is needed beyond filing your return correctly.

Here’s a concrete example of how this plays out:

- Your total solar credit is $9,000

- Your federal tax liability in year one is $6,000

- You apply $6,000 of the credit and bring your liability to zero

- The remaining $3,000 carries forward to the next tax year

- In year two, you apply the $3,000 against that year’s liability

Most homeowners with standard W-2 income clear their full credit within two tax years using this carryforward process.

When a low tax liability becomes a real concern

The carryforward protects you across multiple years, but it does have a practical limit. If your federal tax liability is consistently low or zero, the credit can take several years to fully absorb, and any portion that remains unused when the credit expires simply disappears. The credit is non-refundable, which means the IRS will not send you a check for any balance that exceeds your total lifetime liability.

Retirees on fixed incomes, part-time workers, and individuals with significant deductions that push their liability close to zero should review their tax situation carefully before committing to a large solar purchase based primarily on the credit. Talking to a CPA before you install gives you a realistic projection of how many years your credit will take to fully apply and whether the credit value actually aligns with what you owe.

Where to go from here

You now have a complete picture of how the federal solar tax credit works, from the 30% calculation to the carryforward provision to what happens when your liability runs short. The credit is straightforward once you understand the mechanics, but the installation itself still requires a licensed, experienced contractor who can document your project costs correctly so you capture every dollar you qualify for at filing time.

Florida homeowners have a genuine window right now. The 30% rate holds through 2032, utility costs continue to rise, and the sun in Southwest and Southeast Florida delivers some of the strongest energy output in the country. Getting a professional estimate puts real numbers in front of you so you can see your credit amount, your payback period, and your long-term savings in one place. Contact Advance Solar & Spa to schedule a no-obligation consultation with our certified solar team.